Buy-to-Let Mortgages Explained – How They Work for Landlords

Investing in property can be a lucrative way to generate income, but for many landlords in the UK, buying a rental property often requires a buy-to-let mortgage. Understanding how these mortgages work is crucial to making informed investment decisions. This guide explains the essentials, from eligibility to repayment options, helping landlords navigate the process with confidence.

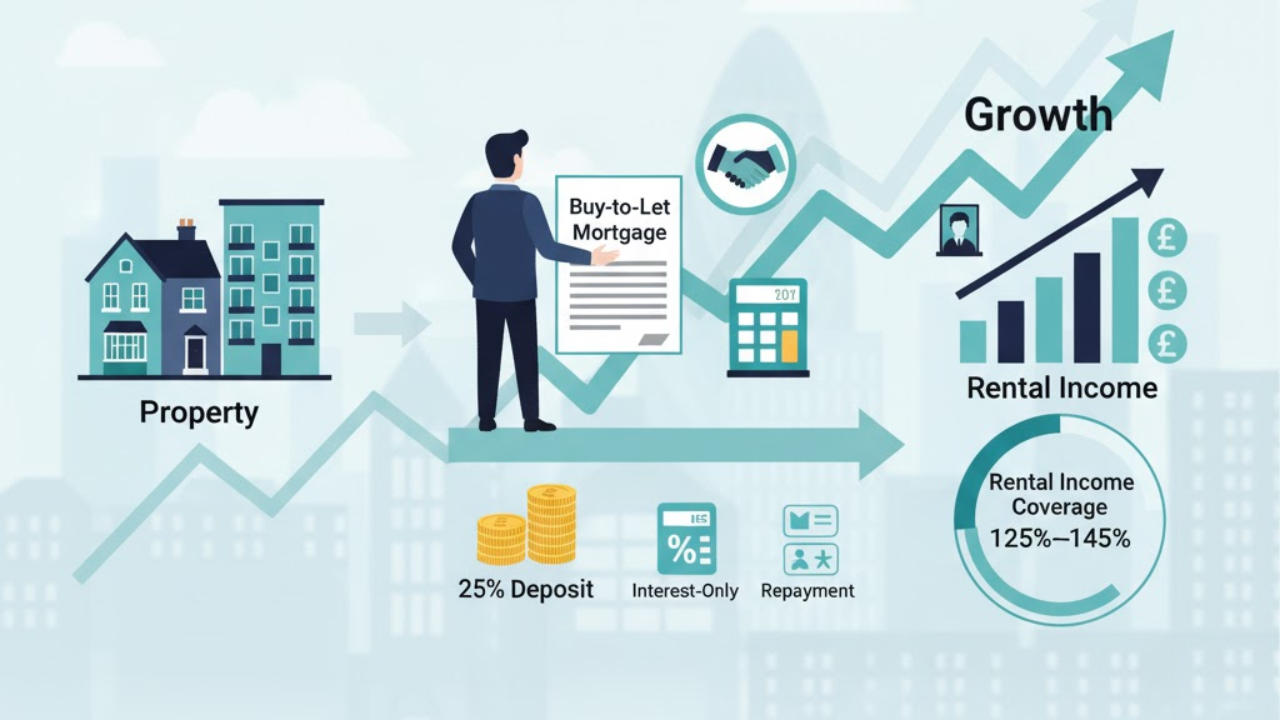

What Is a Buy-to-Let Mortgage?

A buy-to-let mortgage is a loan taken to purchase a property specifically for rental purposes, rather than personal occupation. Lenders focus more on the property’s potential rental income instead of the borrower’s personal income because rental income is what covers the mortgage payments.

Key Features:

- Higher interest rates: Buy-to-let mortgages generally carry higher rates than residential mortgages due to higher risk.

- Larger deposit requirements: Most lenders require at least a 25% deposit — sometimes up to 40%.

- Interest-only repayment options: Many landlords choose interest-only mortgages to keep monthly payments low.

- Strict eligibility criteria: Lenders assess credit history, age, property type, rental demand, and landlord experience.

How Buy-to-Let Mortgages Work

When applying, lenders assess whether the property can generate enough rental income. Typically, rental income must cover at least 125%–145% of the monthly mortgage payments.

Example:

If your mortgage payment is £800 per month, lenders may require projected rental income between £1,000 and £1,160. This ensures you can still manage payments during interest rate rises or vacancy periods.

Lenders also evaluate the property type, location, and local rental demand. High-demand areas offer better mortgage terms.

Types of Buy-to-Let Mortgages

1. Repayment Mortgages

You repay both interest and capital monthly. By the end of the term, the mortgage is fully paid off. This option gives long-term financial security.

2. Interest-Only Mortgages

You pay only the interest each month. The capital is repaid by selling or refinancing the property. This option offers lower monthly payments.

3. Fixed-Rate Mortgages

The interest rate stays the same for an agreed period, keeping monthly payments stable — useful during rising interest rate conditions.

4. Variable-Rate Mortgages

The interest rate fluctuates based on the lender’s SVR (Standard Variable Rate). Initial rates may be low, but payments can increase if the SVR rises.

Eligibility Criteria for Landlords

To qualify for a buy-to-let mortgage in the UK, lenders typically require:

- Minimum age: 21 years

- Minimum income: £25,000+ for first-time landlords

- Good credit history

- Deposit of 25%–40% of property value

Lenders may also evaluate property location, size, demand, and landlord experience — experienced investors get better rates.

Benefits of Buy-to-Let Mortgages

| Benefits | Description |

|---|---|

| Passive Income | Rental payments provide a steady income stream. |

| Capital Growth | Property values may increase over time. |

| Tax Advantages | Mortgage interest and expenses may be tax-deductible. |

| Portfolio Diversification | Reduces reliance on other investment types. |

Risks to Consider

- Interest rate fluctuations: Rates may rise, increasing payments.

- Void periods: Empty periods reduce cash flow.

- Maintenance costs: Repairs and upkeep can be expensive.

- Regulatory changes: Tax or landlord law changes can affect profitability.

Tips for Prospective Landlords

- Research the rental market: Identify high-demand areas.

- Calculate rental yield: Ensure rental income covers all expenses.

- Plan long-term: Look for properties with potential for capital appreciation.

- Use a mortgage broker: They help secure better deals and navigate lender requirements.

- Prepare for unexpected costs: Budget for voids, repairs, and interest rate changes.

Step-by-Step Process to Get a Buy-to-Let Mortgage

- Assess your financial situation — income, credit score, deposit.

- Compare mortgage options — fixed, variable, interest-only, repayment.

- Get a Mortgage in Principle (MIP).

- Choose a suitable rental property based on demand and location.

- Submit a formal mortgage application with required documents.

- Complete the purchase after approval and legal checks.

Final Thoughts

A buy-to-let mortgage is a powerful tool for growing a property portfolio and earning rental income. By understanding how these mortgages work, the risks, and eligibility requirements, landlords can make smart decisions. With careful planning, market research, and expert advice, you can maximise returns and reduce financial risks — whether you’re a first-time landlord or an experienced investor.