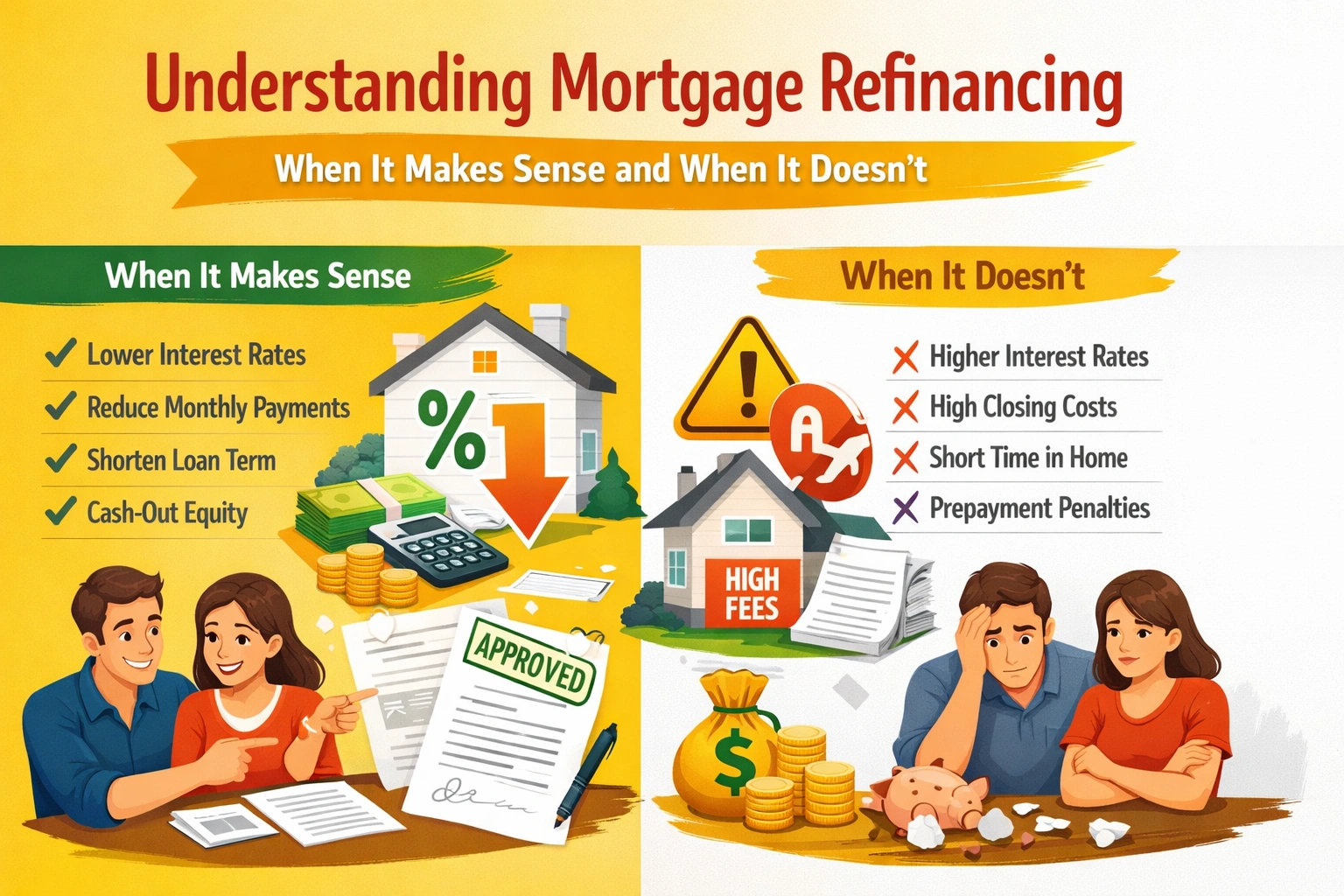

Understanding Mortgage Refinancing

Understanding Mortgage Refinancing