The Complete Guide to Remortgaging Your Property in 2026

If you’re a homeowner in the UK, remortgaging could be one of the smartest financial decisions you make in 2026. Whether you want to reduce your monthly payments, release equity for home improvements, or secure a better deal before your current mortgage expires, refinancing your mortgage can help you reshape your financial future.

But how does the remortgage process really work? What will lenders look for? And is 2026 the right time to switch?

In this remortgage UK guide, we will address all the essential questions you need to know about remortgaging in the UK in 2026.

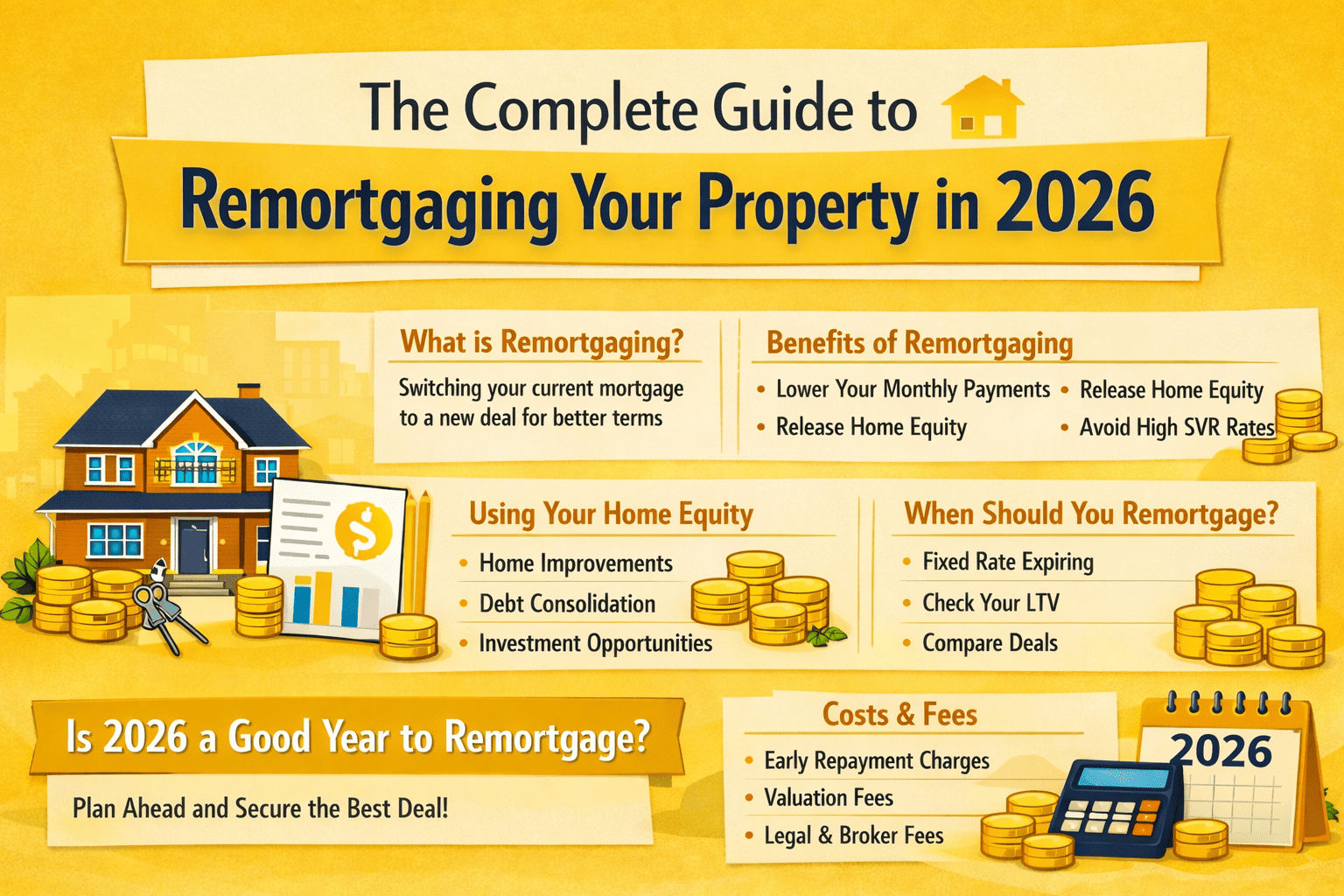

What is Remortgaging?

Remortgaging means replacing your current mortgage with a new one. You can do this with your existing lender or a new one, depending on your choice.

Most homeowners remortgage when their introductory fixed or tracker rate ends. Without a new deal, lenders automatically move borrowers to a Standard Variable Rate (SVR), usually more expensive and unpredictable.

Key Benefits of Remortgaging:

- Lower monthly repayments (if interest rates are better)

- Access to new mortgage features (e.g. overpayment options)

- Ability to borrow more money against your equity

- Avoid expensive SVR rates once your deal expires

- Consolidate higher-interest debts under one secured loan

What is Home Equity & How Can You Use It?

Home equity is the portion of your home that truly belongs to you. It is the difference between your home’s current market value and the amount you still owe on your mortgage.

Home Equity Formula:

Home Equity = Home Value – Mortgage Balance

Example:

Property Value: £350,000

Outstanding Mortgage: £200,000

Equity: £150,000

Through remortgaging, you can release a portion of that equity as a cash-out loan. Many UK homeowners use equity for:

- Renovations & extensions (lofts, kitchens, bathrooms)

- Business investment

- Children’s education

- Buying another property (holiday let / buy-to-let)

- Debt consolidation

When Should You Remortgage?

Timing matters. Most UK lenders allow you to secure a new deal up to 6 months before your current one ends.

- Your fixed-rate deal expires this year

- Your property value has increased

- Market interest rates are lower

- Your financial situation has improved

- You need additional borrowing at lower rates

Avoid switching too early if your lender charges a high Early Repayment Charge (ERC). Always review your mortgage statement first.

The Remortgage Process Step-by-Step

1. Review Your Current Mortgage

Check your rate, remaining term, fees, and any early repayment charges.

2. Check Your LTV (Loan-to-Value)

Mortgage £200,000 ÷ Property Value £350,000 = 57% LTV (Strong position).

3. Compare Deals or Speak to an Advisor

A broker can help you access rates from multiple lenders.

4. Get a Mortgage in Principle

This confirms estimated borrowing eligibility.

5. Valuation & Affordability Checks

Lenders assess income, credit history, and property value.

6. Legal Work & Completion

A solicitor handles legal checks and repays your old lender. Completion typically takes 4–8 weeks.

Costs & Fees to Consider

| Cost | Estimated Amount |

|---|---|

| Early Repayment Charges | 1%–5% of outstanding balance |

| Valuation Fees | Often free with remortgage deals |

| Arrangement/Product Fees | £0–£2,000 |

| Legal Conveyancing Fees | £250–£500 |

| Broker Fees | £0–£600 |

Will Remortgaging Save You Money?

Even a 1% interest rate drop can save thousands over time.

Example:

£200,000 mortgage

25-year term

Rate drop from 5.5% to 4.5%

Savings ≈ £120 per month (£1,440 per year / £36,000+ lifetime)

Remortgage vs Product Transfer

| Option | Meaning | Best When |

|---|---|---|

| Remortgage | Switch to a new lender | You want better rates or equity release |

| Product Transfer | New deal with same lender | You prefer a faster, simpler process |

Is 2026 a Good Year to Remortgage?

Many UK homeowners who fixed during higher-rate periods are reviewing their options as markets stabilise. Rising property values may increase equity and improve eligibility for competitive rates.

Final Thoughts

Your mortgage is likely your biggest lifetime expense. Reviewing it regularly is a smart financial strategy. Remortgaging can reduce pressure, unlock equity, and protect you from high SVR rates.

FAQs

Is remortgaging worth it in 2026?

Yes, if it lowers payments, releases equity, or avoids high SVR rates.

What credit score do you need?

A good score (660+) is typically needed for competitive rates.

How long does remortgaging take?

Usually 4–8 weeks from application to completion. Starting early helps ensure a smooth process.